Large Cap Funds vs Nifty 100 – Are We Comparing Apples to Apples?

- Shwealth

- Feb 12

- 4 min read

When evaluating the performance of large cap mutual funds, we typically compare them against the Nifty 100 Index, which serves as their official benchmark. This makes sense on paper — after all, SEBI mandates that large cap funds must invest at least 80% of their portfolio in the top 100 companies by market capitalization, represented by the Nifty 100 universe.

However, this comparison isn’t entirely apple-to-apple. Large cap funds are allowed to invest up to 20% of their corpus in mid cap and small cap stocks. Over the past decade, midcaps and smallcaps as a category have outperformed the Nifty 100, allowing fund managers who tactically allocate to these segments to generate alpha over the benchmark. This makes it important to question whether the Nifty 100 truly reflects the risk-adjusted performance of large cap funds.

A Hypothetical Benchmark: Nifty 100 + Midcap 150

To test how much of this outperformance comes from exposure beyond large caps, we can construct a hypothetical blended benchmark — made up of:

85% Nifty 100, and

15% Nifty Midcap 150.

Why 85% and not 80%? Because 80% is the minimum mandated allocation to large caps; in practice, most large cap funds maintain around 85–90% in large caps and 10–15% in midcaps. This mix provides a more realistic representation of how large cap portfolios are typically structured.

For this analysis, I compared the performance of leading large cap funds such as Nippon, SBI, Kotak, ICICI, Canara Robeco, Mirae, Invesco and HDFC— all of which have consistently delivered above-average returns relative to the Nifty 100. Other funds that have failed to consistently beat the benchmark over time have been excluded from the comparison.

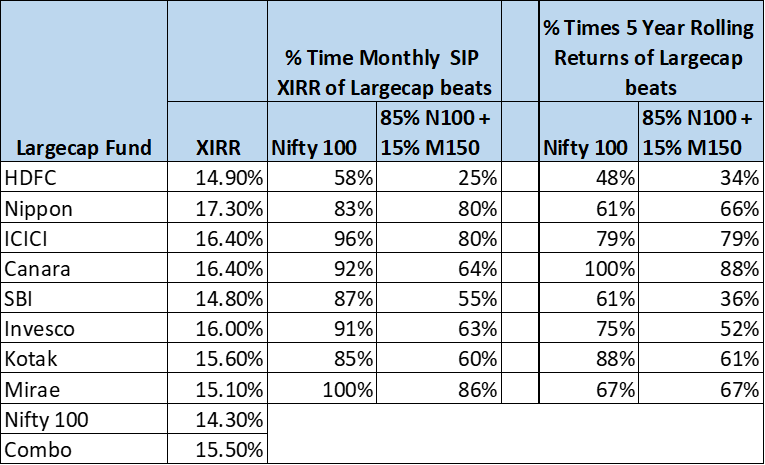

Table 1: Large caps performance vis-à-vis Nifty 100 and Combination of 85% Nifty 100% and 15% Midcap 150 index – Jan 2014 to June 2025

Note: Returns of the blended index do not include any fund management charges, since base data is of the two index itself

The Results

For looking at consistency, we have compared both SIP returns over the given period as well 5 year rolling returns. The SIP returns would be comparing 138 data points (i.e. 138 months from Jan 2014 to June 2025). Rolling returns would be comparing over 2,300 data points. Rolling returns and SIP returns for the blended index have been calculated using our in-house MF portfolio builder.

As shown in Table 1, the consistency of outperformance naturally reduces when compared to the weighted benchmark. HDFC and SBI show a significant drop in consistently beating the blended index compared to just Nifty 100, while Nippon and ICICI largecap shine even when compared to the blended index. The remaining schemes also show good consistency in beating the blended benchmark. This demonstrates that their outperformance may not be a result of taking additional midcap exposure, but stems from genuine active fund management, strong stock selection, and portfolio construction within the large cap universe.

So, Should You Choose an Index or a Large Cap Fund?

The real question isn’t simply whether investors should choose the Nifty 50, Nifty 100, or an actively managed large cap fund. It’s about aligning investments with the investor’s desired market exposure, volatility comfort, and risk-return objectives.

If an investor prefers pure large cap exposure — strictly the top 50 or 100 companies — then index funds tracking Nifty 50 or Nifty 100 may be the most suitable choice.

If an investor is comfortable with limited midcap exposure and seeks moderate alpha generation through active management, then large cap mutual funds can be a more rewarding option.

On the other hand, if an investor already holds midcap or small cap funds, adding an actively managed large cap fund may result in portfolio overlap. In such cases, sticking to a passive index fund for the large cap allocation could be more efficient.

Conclusion

While the Nifty 100 Index remains the official benchmark for large cap funds, a blended benchmark (such as 85% Nifty 100 + 15% Nifty Midcap 150) offers a fairer and more nuanced picture of true fund performance. Certain large cap funds continue to outperform even after adjusting for midcap exposure.

Ultimately, the decision between index investing and actively managed mutual funds should depend on an investor’s asset allocation strategy, risk appetite, and return expectations — not merely on historical outperformance against a single benchmark.

Data Source: Base NAV data taken from www.advisorkhoj.com. Data analyzed through our in-house MF model for returns of individual schemes and portfolio.

Disclaimer- This is not a recommendation to invest in any of the instruments mentioned in the article. Nothing in the article is my solicitation, recommendation, endorsement, or offer. If you have any doubts as to the merits of the article, you should seek advice from an independent financial advisor. or tax advisor. Registration granted by SEBI, BASL membership, and NISM certification does not guarantee the intermediary’s performance or provide any assurance of returns to investors. Investment in the securities market is subject to market risks. Read all the related documents carefully before investing.

Comments